News

How to know the code of goods and services for 10% or 8% VAT invoice

To know if an enterprise can apply the value-added tax (VAT) rate of 8% according to Decree No. 15/2022/ND-CP, it is necessary to check the code of goods and services. Viet Australia Auditing Ltd guides the steps to look up the code of goods and services as follows:

- Step 1: List the products that the business is actually manufacturing, trading... that generates revenue and VAT invoices

- Step 2: Open Decision No. 43/2018/QD-TTg dated November 1, 2018 to check the name of your goods and services in step 1. What is the corresponding product code?

- Step 3: Take the product code found in step 2 and compare it with the code of goods and services specified in Appendix I, Appendix II and Appendix III of Decree No. 15/2022/ND-CP:

- If codes of goods and services are identical: Enterprises are not entitled to incentives. 10% VAT invoices applied.

- If codes of goods and services do not match: Enterprises receive incentives, 8% VAT invoices applied.

The checking of the economic sector code is for the purpose of comparing the list of goods and services in 13 sectors that cannot apply VAT reduction according to the provisions of Decree No. 15/2022/ND-CP.

To know what is the business code of the Enterprise in case the Enterprise deals in multiple product codes, you can check at the following address (check by entering the tax code) >>> CHECK HERE

In addition, to be accurate, you can look up details at Decision No. 43/2018/QD-TTg dated November 1, 2018 to look up new product and service codes. can be accurate.

1. Telecommunications - Details can be found at: Appendix III

2. Financial activities - Details can be found at: Appendix I

3. Banking - Details can be found at: Appendix I

4. Securities - Details can be found at: Appendix I

5. Insurance - Details can be found at: Appendix I

6. Real estate business - Details can be found at: Appendix I

7. Metal and prefabricated metal products - Details can be found at: Appendix I

8. Mining products (excluding coal) - Details can be found at: Appendix I

9. Coke coal - Details can be found at: Appendix I

10. Refined petroleum - Details can be found at: Appendix I

11. Chemicals and chemical products - Details can be found at: Appendix I

12. Products and goods subject to excise tax - Details can be found at: Appendix II

13. Information technology under the law Information technology - For details, see Appendix III

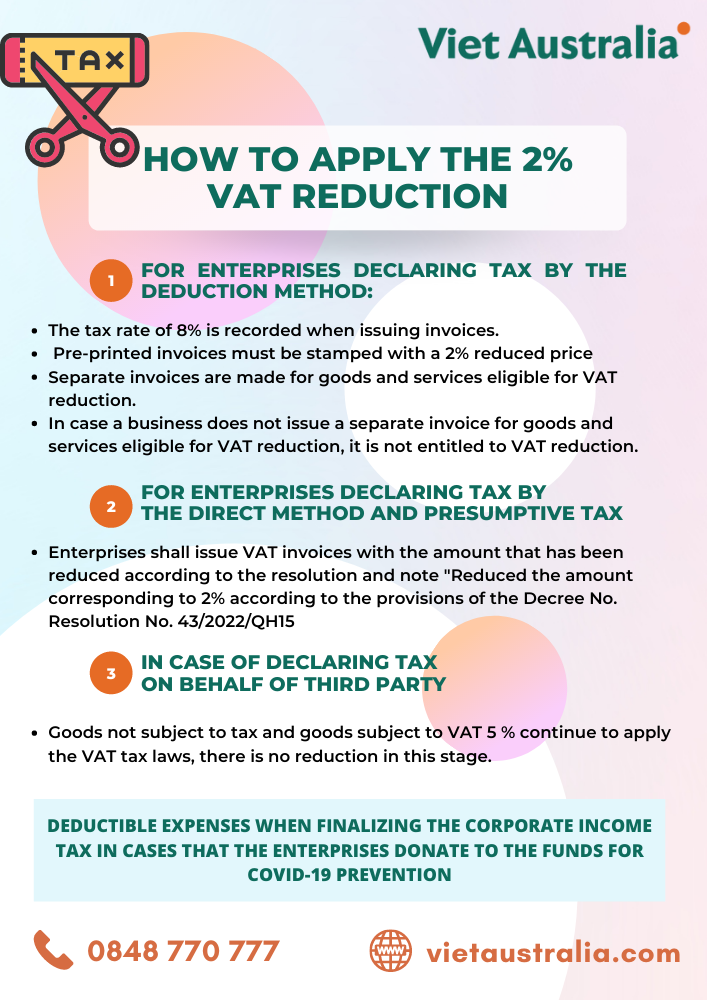

How to apply the 2% VAT reduction

1. For enterprises declaring tax by the deduction method:

The tax rate of 8% is recorded when issuing invoice.

Pre-printed invoices must be stamped with 2% reduced price

Separate invoice are made for goods and services eligible for VAT reduction.

In case a business does not issue a separate invoice for goods and services eligible for VAT reduction, it is not entitled to VAT reduction.

2. For enterprises declaring tax by the direct method and presumptive tax

Enterprises shall issue VAT invoices with the amount has been reduced according to the resolution and note "Reduced the amount corresponding to 2% according to the provisions of the Decree No. Resolution No. 43/2022/QH15

3. In case of declaring tax on behalf of the third party:

It must attach Form No. 01 in Appendix IV issued with this Decree together with the VAT declaration. Goods not subject to tax and goods subject to VAT 5 % continue to apply the VAT tax laws, there is no reduction in this stage.

In addition, the Decree provides detailed instructions on the calculation of deductible expenses when finalizing the corporate income tax in cases that the enterprises donate to the funds for Covid-19 prevention and control that the following agencies call for:

- Vietnam Fatherland Front Committees at all levels;

- Medical facilities;

- Armed forces units;

- Units and organizations assigned by competent state agencies to act as concentrated isolation facilities

- Educational institutions; press agencies;

- Ministries, ministerial-level agencies, Governmental agencies;

- Party organizations, youth unions, trade unions and unions of Vietnamese women at all levels at central and local levels;

- Local government agencies and units at all levels have the function of mobilizing funding; - Fund for Covid-19 pandemic prevention and control at all levels;

- Fund for vaccines against Covid-19;

- National humanitarian portal; Charity and humanitarian funds and organizations with the function of mobilizing funding are established and operate in accordance with law.

Other News

Contact Infomation

Viet Australia Auditing

Viet Australia Auditing Company is a professional audit firm providing audit services, tax services, business consulting services in Vietnam. Viet Australia Auditing recruited among professionals coming from the Big4 such as PWC and Deloitte.

HOTLINE: 0848770777

- Head Office: Level 7, 25 Restwell street, Bankstown NSW 2200

- Trading Address: 25B Hoang Dieu Street, Phu Nhuan Ward, Ho Chi Minh City, Vietnam

- Phone: 028 3925 1360

- Mail: info@vietaustralia.com

- Fax: 028 3925 1359

- https://www.linkedin.com/company/vietaustralia/

© 2007 - Viet Australia Auditing Ltd. All rights Reserved