News

New Key guidance in Decree 126/2020 on Tax administration from 5th December 2020

05 cases are not required to submit tax declaration dossiers as follows:

Taxpayers are not required to submit tax declaration dossiers in the following cases:

1. Taxpayers only conduct activities and do business belongs to Non-taxable objects according to the provisions of tax law applicable to each type of tax;

2. Individuals have Tax-exempt incomes under the law on personal income tax and at Point b, Clause 2, Article 79 of the Law on Tax Administration, except individuals who receive real estate inheritance or gifts; real estate transfer;

3. An export processing enterprise only engaged in export activities is not required to submit value-added tax declaration dossiers;

4. Taxpayers suspend operations or business in accordance with Article 4 of this Decree 126/2020;

5. Taxpayers shall submit dossiers of tax identification number deactivation, except for termination of operation, contract termination or reorganization of enterprises according to the provisions of Clause 4, Article 44 of the Law on Tax Administration.

(Current regulations in Decree 83/2013 / ND-CP do not mention this issue.)

Additional guidance on coercive measures to enforce administrative decisions on tax administration

The Law on Tax Administration 2019 adds coercive measures to work out decisions on tax administration, as follows:

“Coercive by the measure of stopping customs formalities for exported and imported goods.”

(Decree 126/2020 has added detailed guidance on this measure compared to Article 19 of Decree 129/2013/ND-CP and its guiding documents)

Not allowed to cancellation of tax debts on land levies, rents for land and water surface, and fees for protection and development of paddy soils

Pursuant to the provisions of Point h, Clause 2, Article 5 of Decree 126/2020/ND-CP Payers of other amount payables to the state budget have had a cancellation of outstanding tax the amount to be remitted into the state budget if falling under the specified circumstances in Article 85 of the Law on Tax Administration, except for the land levies or rents for land and water surface and fees for protection and development of paddy soils.

Dossiers, authorization and responsibility for the application form cancellation of tax debts follow provisions on Articles 86, 87, and 88 of the Law on Tax Administration.

So, the taxpayer will not be able to allowed to cancellation of tax debts on land levies, rents for land and water surface, and fees for protection and development of paddy soils under any circumstances.

(Currently, on Clause 3, Article 48 of Circular 156/2013/TT-BTC only regulation for not allowed to cancellation of tax debts on land levies, rents for land, debt cancellation for land levies and land rental are done according to regulations in the Land Law and documents guiding the implementation of the Land Law).

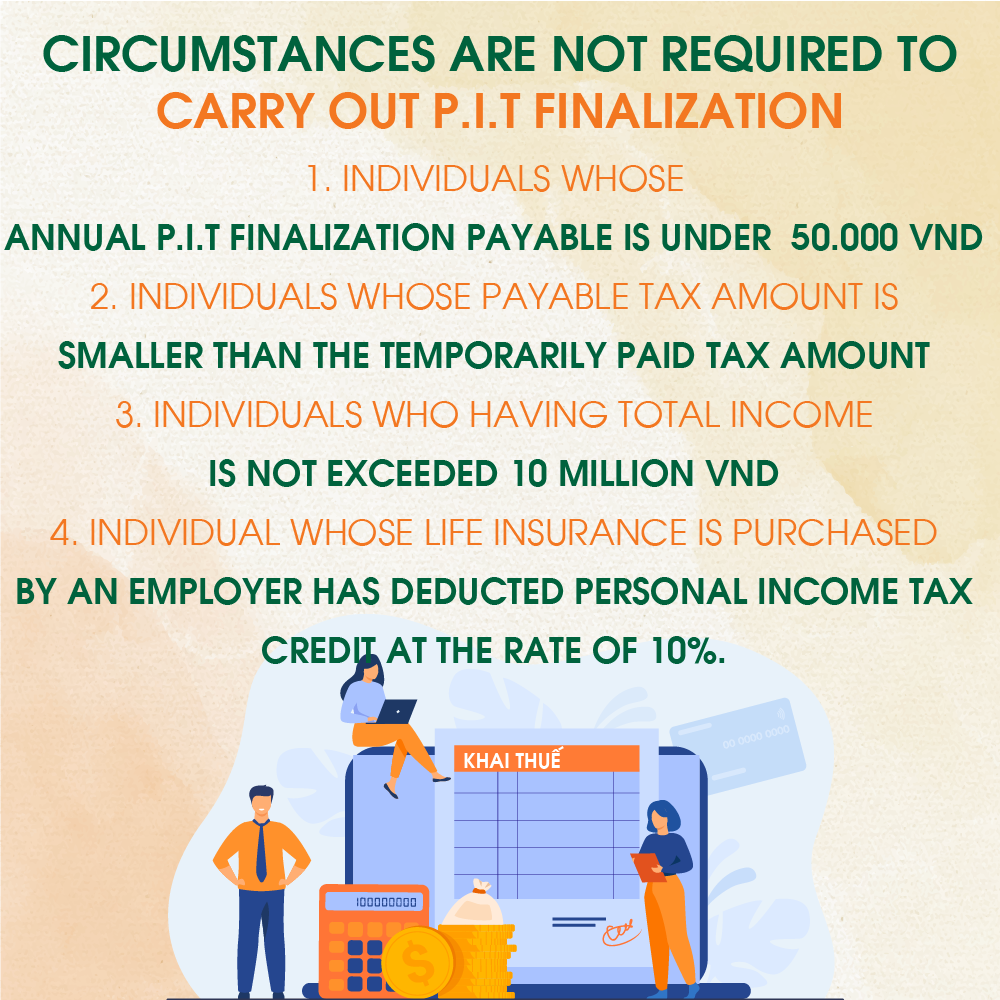

Circumstances are not a resident individual with income from salaries or wages are not required to carry out PIT finalization

Pursuant to Point d.3 Clause 6 Article 8 of Decree 126/2020/ND-CP except for cases as follows:

1. Individuals whose annual personal income tax payable on salary or wage is VND 50.000 or smaller (news);

2. Individuals whose payable tax amount is smaller than the temporarily paid tax amount without claiming tax refund request or offset into the next tax return period;

3. Individuals who having income from salaries or wages have signed labor contracts from 03 months or more in a company, and have current income in other places on average monthly in the year not exceeding 10 million VND and have received personal income tax credit at the rate of 10%. If there is no request, tax finalization is not required for this income;

4. An individual whose life insurance is purchased by an employer (except pension non-compulsory insurance) or other non-compulsory insurance with the accrual of insurance fees that the employer or insurance company has deducted Personal income tax credit at the rate of 10% on the insurance fees corresponding to the part that the employer buys or contributes to the employee, the employee is not required to finalize personal income tax on this income (new).

(Compare with Article 12 of Circular 151/2014 / TT-BTC)

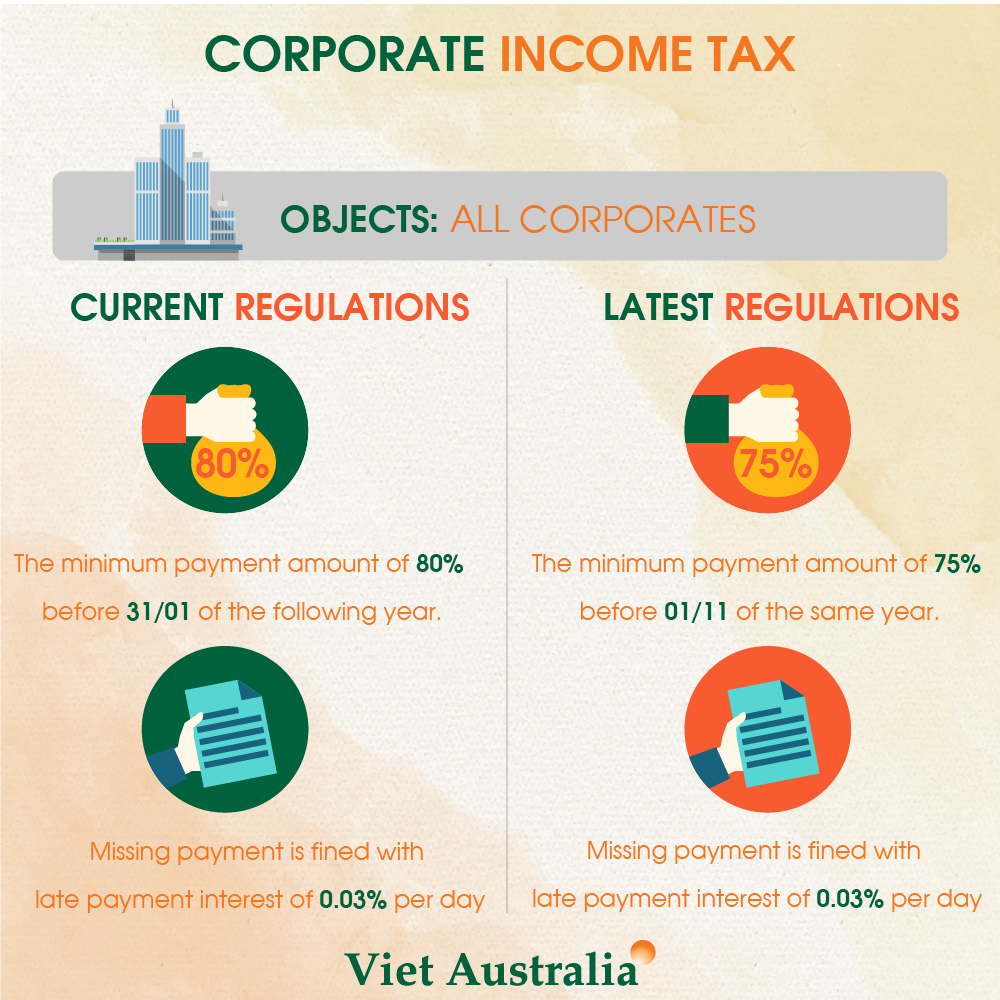

Payment of Corporate Income Tax in the first 3 quarters of a tax year must not be less than 75% of the total CIT of the year

According to the provisions of Point b, Clause 6, Article 8 of Decree 126: The total amount of provisional CIT paid in the first 3 quarters of a tax year must not be less than 75% of the total CIT liability for the year based on tax finalization.

If the provisional quarterly CIT payments in the first 3 quarters account for less than 75% of the final CIT liability, late payment interest will impose on the shortfall, calculating from the due date of the provisional payment for the third quarter until the settlement date.

Banks are required to provide customer account details at the request of the tax authorities

According to Clause 2, Article 30 of Decree 126, at the request of tax administration agencies, commercial banks provide information on each taxpayer's payment account, including:

+ Account holder name;

+ Account holder number according to the individual’s tax code issued by the tax authority;

+ Date of account opening, date of account closure.

The provision of account information as regulations above will be done for the first time within 90 days from 05th December 2020, account information is updated monthly for 10 days of the next month.

Commercial banks provide transaction information via accounts, account balance, transaction data at the request of the Head of the tax administration agency to serve the purpose of inspection, examination, determination of payable tax obligations, and implementation of coercive measures to enforce decisions administration on tax administration in compliance with provisions on taxation.

Tax administration agencies are responsible for protecting confidentiality of information and fully responsible for the safety of information in compliance with the law.

(Current regulations in Decree 83/2013/ND-CP do not mention this issue)

Specific provisions on tax declaration and payment of tax on behalf of individuals receiving stock dividends

Decree 126 stipulates the organization of tax return and tax payment on behalf of individuals receiving stock dividends, individuals who are existing shareholders receiving stock rewards; individuals are recognized for the capital increase due to income recorded capital increase; Individuals contributed capital with real estate, capital contribution, securities as follows:

+ For individuals receiving stock dividends by securities: If an individual is an existing shareholder receiving a prize in securities, the organization shall declare tax and pay tax on behalf of the individual on income from the capital investment when the individual transferring securities of the same type.

+ For securities through the trading system on the Stock Exchange: the organization substitute that declares and pays tax is the securities company or commercial bank where the individual opens depository accounts, fund management companies where the individual entrusts the portfolio.

+ For securities that do not pass the trading system on the Stock Exchange: the organization shall declare tax and pay the tax instead as follows:

For securities of public companies that have registered securities at the Securities Depository Center, the organization substitute that declares and pays tax is the securities company or the commercial bank where the individual opens the securities depository account.

Securities of a Joint-stock company which has not a public company yet, but the issuing organization authorize a securities company to manage the list of shareholders, the organization substitute that declares tax and pays tax is an authorized securities company permission; For securities that are not subject to the provisions of this clause, the organization substitute that declares tax and pays tax is the issuing securities organization.

+ For an individual whose capital increase is recognized due to an increase in his/her increased profits gains, the organization substitute where he/she has contributed capital shall declare tax and pay tax for the individual on the income from capital investment when transfer or withdraw capital.

+ For individuals contributing capital with real estate, capital contribution, or securities, the organizations substitute where they contribute capital shall declare tax and pay tax for them on income from the real estate transfer, and income from the capital transfer, income from securities transfer.

Specifying the regime of tax declaration and payment on behalf of individuals receiving stock dividends

According to Point d, Clause 5, Article 7 of Decree 126, for individuals receiving stock dividends; an individual who is an existing shareholder receives a stock reward, so the organization is responsible for declaring tax and paying tax on behalf of individuals for income from the capital investment when individuals transfer securities of the same type...

Thus, instead of self-declaration, the organization is responsible for declaring and paying tax on behalf of the individual receiving stock dividends; Individuals who are existing shareholders receive securities rewards, individuals are recognized for the capital increase due to increased profits gains.

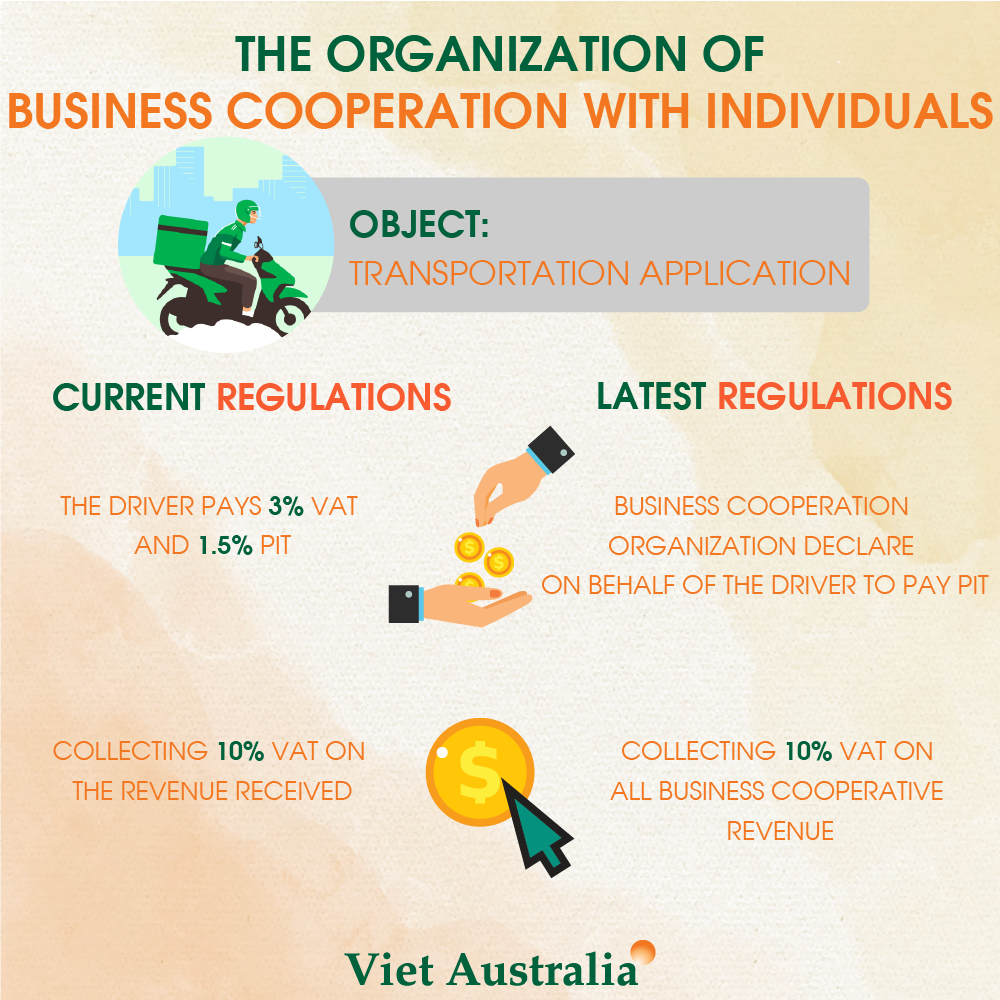

In the case of organizations business cooperating with individuals, individuals do not directly declare tax

Point c, Clause 5, Article 7 of Decree 126 states: “If an organization co-operates with an individual, the individual does not directly declare tax”. Organizations are responsible for declaring value-added tax on all revenue from business cooperation activities in accordance with the tax law and tax administration, irrespective of the form of division of results business cooperation, and at the same time, declare and pay on behalf of personal income tax for individuals doing business.

In the case of the business organizations and individuals are being household business or individual business according to Clause 5, Article 51 of the Law on Tax Administration, the individual has business cooperation that is the same business line with the organization, the organization and individual shall declare tax by themselves corresponding to the actual results of business cooperation as regulated.

Detailed guidance on locations to submitting the tax declaration dossier for taxpayers who have many activities and businesses in many provincesAccording to Clause 1, Article 11 of Decree 126/2020/ND-CP the locations to submitting the tax declaration dossier for taxpayers who have many activities and businesses in many provinces that are tax authorities where business activities are conducted in different locations of province or city where the head office is located in the following cases:

1. Declaring value-added tax on investment projects in the case specified at Point d, Clause 2, Article 7 of Decree 126 at the locality where the investment project is located.

2. Declaring value-added tax on real estate transfer of infrastructure investment projects, houses for transfer (including the case of received advances of payment from customers according to progress) at locations where the real estate transfer is activated.

3. Declaring value-added tax on where there are power stations.

4. Declaring excise tax where the place of production or processing of goods subject to excise tax or service provider subject to excise tax (except for the business of lottery calculator).

In case the taxpayer directly imports goods subject to excise tax and then sells it in domestic, the taxpayer must declare excise tax with the

directly managed tax authorities of the locality where the taxpayer is headquartered.

5. Declaring environmental protection tax at the place where produced of taxable goods for environmental protection, except for the environmental protection tax of petroleum business activities as specified in Point a Clause 4 Article 11 of Decree 126.

6. Declaring environmental protection tax at the place where the coal production and trading establishment is located (including internal consumption), except for the environmental protection tax specified at Point b, Clause 4, Article 11 of Decree 126.

7. Declaring natural resource consumption tax (except for natural resource consumption tax for hydropower production in case hydropower's lake bed of hydroelectric power plants is located in the same areas of provinces; crude oil exploitation and export; exploitation and sale of natural gas and the natural resource tax of the organization assigned to sell the captured or confiscated resources; irregular natural resource exploitation has been licensed by a competent state agency or is not subject to a license in compliance with provisions on the law).

8. Declaring Corporate income tax at the places of dependent units, place of business has income and receive preferential treatment on corporate income tax.

9. Declaring the environmental protection fee at the places of mineral extraction site (except for crude oil, natural gas, and coal gas; organize the collection of minerals from small miners).

10. Declaring the license fee at the place of the dependent unit or place of business activities.

Other News

Contact Infomation

Viet Australia Auditing

Viet Australia Auditing Company is a professional audit firm providing audit services, tax services, business consulting services in Vietnam. Viet Australia Auditing recruited among professionals coming from the Big4 such as PWC and Deloitte.

HOTLINE: 0848770777

- Head Office: Level 7, 25 Restwell street, Bankstown NSW 2200

- Trading Address: 25B Hoang Dieu Street, Phu Nhuan Ward, Ho Chi Minh City, Vietnam

- Phone: 028 3925 1360

- Mail: info@vietaustralia.com

- Fax: 028 3925 1359

- https://www.linkedin.com/company/vietaustralia/

© 2007 - Viet Australia Auditing Ltd. All rights Reserved